"We Back People, Not Ideas" Is the Biggest Lie in AI Investing | SVTR Thesis

There’s a line that gets repeated in venture capital like a prayer: “We invest in people, not ideas.”

It’s a beautiful line. It casts the investor as a talent scout with preternatural instincts, places the founder at the center of the story, and wraps every check in a narrative about betting on human potential. It’s gospel in Silicon Valley. It’s even more so in the official talking points of China’s top-tier VC firms. But here’s what we believe at SVTR: in today’s AI investing landscape, this phrase has degraded from a philosophy of judgment into the single biggest fig leaf covering the industry’s most systematic failures — and the bill is coming due at an alarming pace.

More precisely, “backing people, not ideas” is no longer a form of judgment. It’s a way of avoiding judgment. When an investor says this, they almost never have to explain what they actually saw. The phrase has three convenient properties: it conforms to industry norms, it doesn’t offend founders, and it requires zero specific argumentation. Naturally, it becomes the perfect cover for every bias, every résumé worship, every shortcut.

A Philosophy Misread for Four Decades

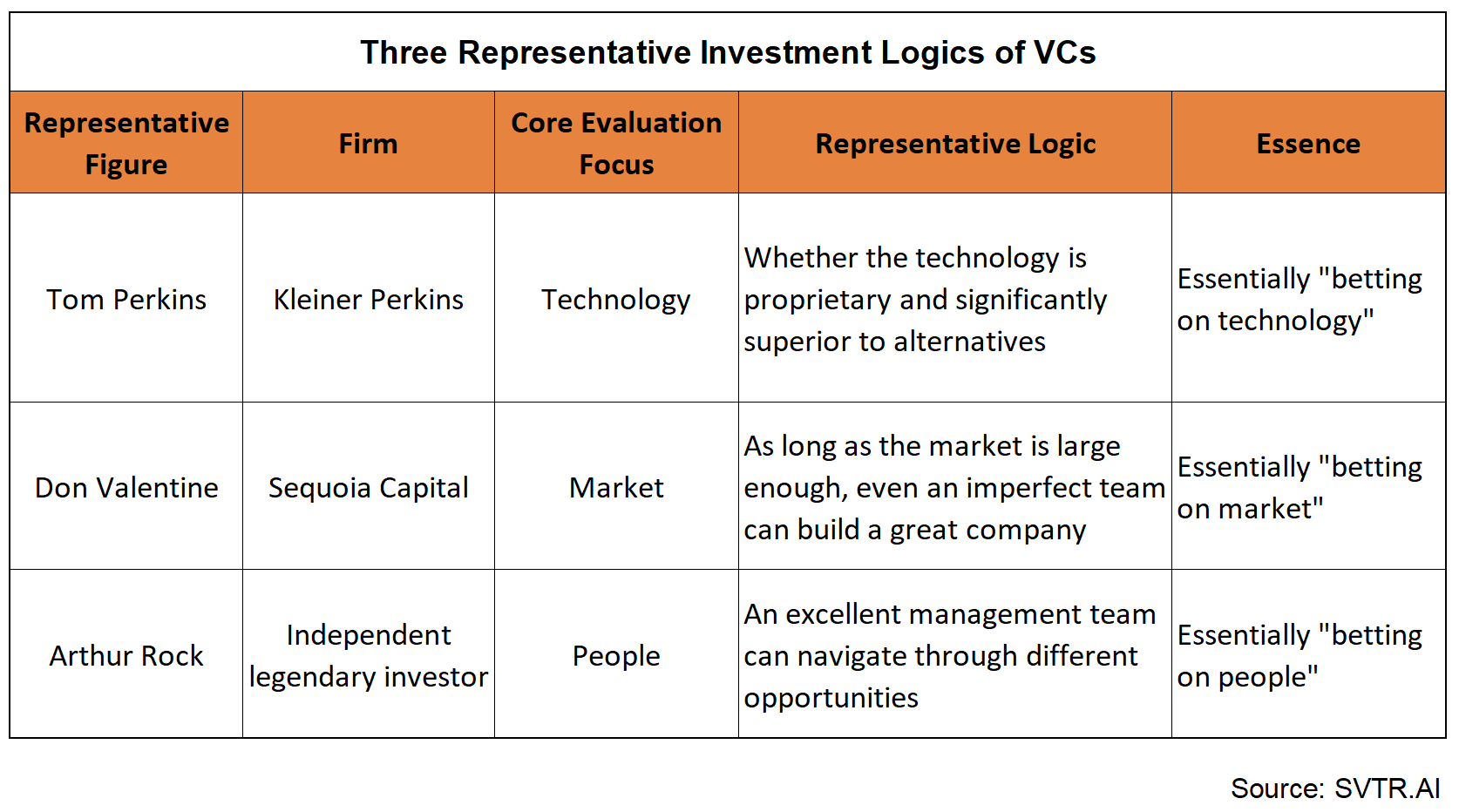

The VC industry didn’t always have a consensus on “backing people.” Tom Perkins at Kleiner Perkins looked at technology — is it proprietary? Is it significantly better than the alternatives? Don Valentine at Sequoia looked at markets — a big enough market, he believed, could carry even a mediocre team. His mid-1980s investment in Cisco happened precisely because peers thought the team was weak, but he was convinced the networking market would lift any decent team. Arthur Rock looked at people — he believed a great management team could navigate any specific opportunity.

Rock’s version won the culture war. The reason isn’t complicated: founder-centric narratives make for better marketing. For funds that are essentially selling capital to founders, “we believe in you“ is exactly what founders want to hear.

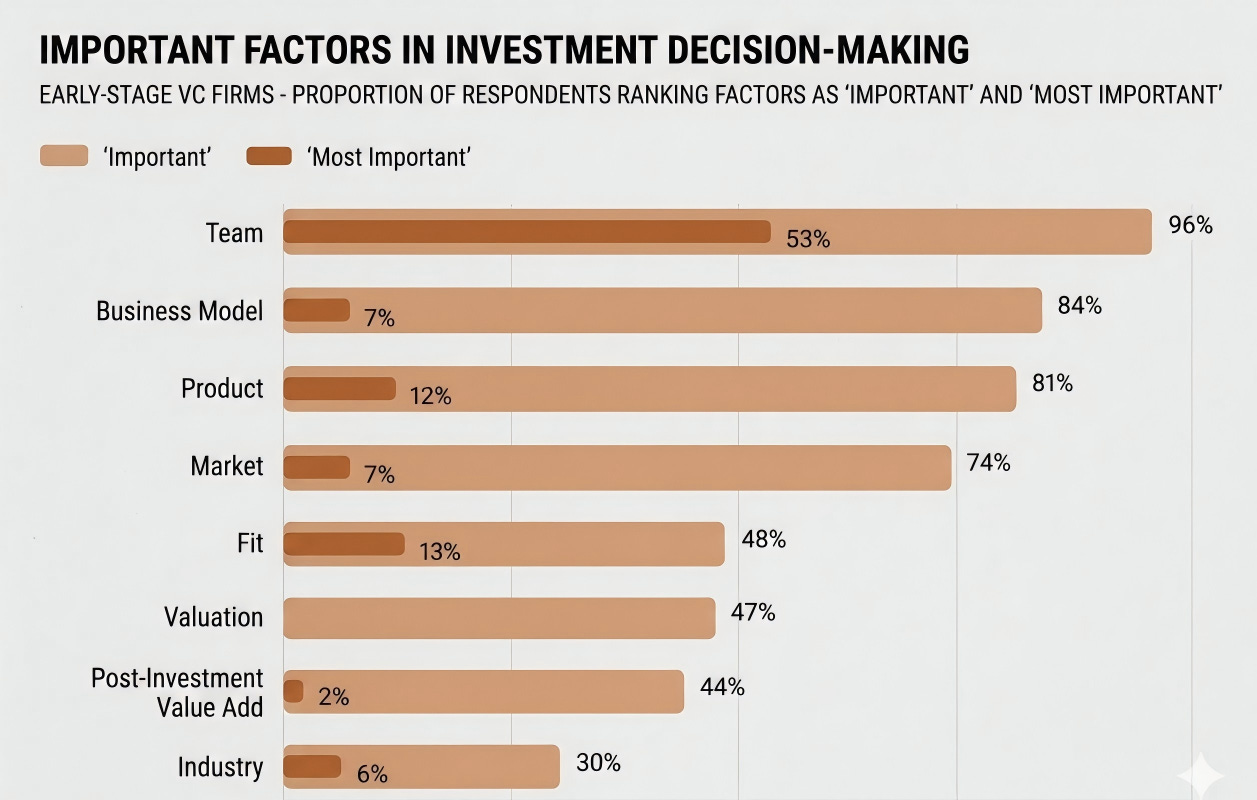

But “backing people” in today’s practice is no longer what Rock meant. A 2016 survey by Gompers, Gornall, Kaplan, and Strebulaev — covering 681 VC firms and 885 investors — found that 96% listed the team as a key factor, 56% considered it the single most important factor, and 17% of early-stage investors admitted they don’t use any financial metrics at all. An industry overwhelmingly reliant on qualitative judgment, yet without any clear articulation of what the criteria are or how to trace them back to outcomes. Scholars Andrew Zacharakis and G. Dale Meyer put it more bluntly: investors don’t actually understand their own decision-making process.

The Historical Tab for “Backing People”

Diag Davenport, an economist at Chicago Booth, ran the numbers on this “fuzzy humanism” in a 2022 study. Using a dataset of over 16,000 startups and more than $9 billion in committed capital, he trained machine learning models using only information available to investors at the time of their decisions, and asked one question: of the deals VCs actually funded, how many could have been identified ex ante as worse than simply putting the same money into public markets?

The answer: roughly half.

If you removed that half and redirected the capital to a public market index, the overall sample returns would have improved by 7 to 41 percentage points — representing over $900 million in avoidable losses.

The more telling finding was Davenport’s parallel experiment. He trained two models side by side: one to predict the best investments, one to predict the worst. The two models relied on entirely different signals. The model predicting great investments leaned heavily on product characteristics. The model predicting terrible investments leaned heavily on founder backgrounds. In other words: when investors made good decisions, they were actually studying the product. When they made bad decisions, they were studying the team even harder.

This isn’t news to the VC industry. But few people are willing to say it out loud: the more energy VCs spend on “backing people,” the more systematically — and expensively — they get it wrong.

Pricing Foundation Models by Résumé

Map this dynamic onto the global AI investing boom since 2023, and it reads like a controlled experiment. China and the U.S. ran nearly identical playbooks, almost in sync.

On the China side, there was Lightyear (光年之外). In early 2023, Wang Huiwen — known as “Meituan’s number two” — announced he was entering the foundation model space. No product. No complete team. He didn’t write code himself. Yet within months, he raised roughly $230 million at a $1 billion valuation, backed by top-tier USD funds and leading PE firms. The money wasn’t invested in a model or any concrete product thesis. It was invested in the three characters of his name. Months later, he stepped down for health reasons, and the company was absorbed back into Meituan. End of story.

On the Silicon Valley side, there was Inflection AI. Mustafa Suleyman (DeepMind co-founder) + Karén Simonyan + Reid Hoffman — that lineup secured $1.3 billion in funding at a $4 billion valuation, the largest early-stage AI round in North America that year. A year later, Microsoft executed a “non-acquisition acquisition,” pulling out the core team almost wholesale, leaving behind a corporate shell that was repurposed into a B2B API business. Adept and Character AI followed nearly identical scripts through 2024, with Amazon and Google as the respective acquirers.

Line these names up and the conclusion is hard to avoid: among the largest, most hotly pursued early-stage AI checks of 2023, a significant portion were not investments in companies at all. They were risk exposure management on a set of résumés. Even before the outcomes materialized, these deals would have been flagged red in Davenport’s model — their entire thesis was a CV.

The more systematic version played out in each market’s “foundation model” cohort. In China, it was the “AI Six Tigers” (六小虎): Moonshot AI, Zhipu, Baichuan, MiniMax, StepFun, and 01.AI. In the West, it was the ring beyond Anthropic and xAI: Mistral, Cohere, Reka, AI21, and others. What these companies had in common wasn’t product form, technical approach, or market positioning — it was the credential layer of their founders: Google Brain, DeepMind, OpenAI, Meta AI, Tsinghua, CMU, Microsoft Research. Within roughly a year, the vast majority crossed the $1 billion valuation threshold — most while product form was far from stable and business models remained unproven. The investment logic was remarkably candid: the people who “look like they should be able to build foundation models” are these people. Résumés are a reasonable weak signal. But they were being priced as a strong one.

The Dark Horses Outside the “Expected” List

Outside this résumé-driven curve, the most globally recognizable AI companies of the past two years happen to be the ones that least fit the “résumé-pricing model.”

In China, it’s DeepSeek. Founder Liang Wenfeng came from the quantitative hedge fund High-Flyer — not a typical Big Tech AI lab pedigree, and not on most investors’ initial mental list of “foundation model founders.” Yet DeepSeek, through V2, V3, and R1, pushed open-source model capabilities to the global frontier, even forcing Silicon Valley to recalibrate its assumptions about model costs, capabilities, and valuation curves.

In Silicon Valley, it’s Midjourney. Founder David Holz came from the world of haptic interaction, not mainstream AI research. The company took no VC money, did no fundraising PR, yet built one of the most successful consumer-facing AI businesses of this entire cycle on the strength of product and distribution alone.

And then there’s Cursor — not a “model lab alumni” narrative, not a founder-résumé media story, but a team that cut into a specific developer workflow and built an AI coding tool with genuinely compelling product experience.

These companies aren’t counterexamples to “backing people.” Quite the opposite — they demonstrate that the people truly worth backing are often not the ones with the shiniest résumés, but the ones who reveal distinctive judgment within a specific problem.

If the “back people” logic holds, what investors should actually be evaluating isn’t where someone came from, but:

Why did they choose this problem?

How do they define this problem?

What counterintuitive but correct trade-offs have they made in the product?

Did they see an opportunity the market hasn’t correctly named yet — and see it earlier than everyone else?

Strip away these questions, and “this person is strong” isn’t backing people. It’s backing labels.

What “Backing People” Actually Looks Like

Peter Thiel’s investment in Mark Zuckerberg is often simplified into “early talent recognition,” but contemporaneous accounts show that what Thiel actually valued wasn’t Zuckerberg as an abstract “person” — it was how he chose to approach the problem of online identity, and the specific form Facebook had already taken. Thiel himself said it plainly at a DealBook conference: he doesn’t evaluate people, ideas, business strategy, and technology separately. It’s a complex whole.

Nabeel Hyatt at Spark Capital makes this even more operational: he never decides whether to write a check by watching a founder present. Instead, he uses the product repeatedly, studies every decision embedded in it, and reverse-engineers the judgment, priorities, and problem-solving approach of the person behind it. Sam Altman, during his YC era, formalized it further as the “non-obvious brilliance of an idea” — not whether the founder is smart, but whether the idea is smartly choosing an underestimated problem. Mattia Bianchi at the Stockholm School of Economics and Roberto Verganti at Politecnico di Milano arrived at the same conclusion from the academic side: the most important creative act in entrepreneurship is not solving problems, but defining them.

Put these voices together and the conclusion is clear: the atomic unit of an investment is neither the founder nor the idea — it’s the fusion of the two. An investor who can’t discuss the team without discussing the problem is either investing in shallow pattern-matching or personal charisma. Both will reliably produce Davenport’s bottom half of “predictably bad investments.”

What’s Actually Scarce in AI Investing

In this AI cycle, capital is the last thing the market lacks. Nor is there a shortage of star founders being chased by that capital. What’s genuinely scarce is a more fundamental capability: the judgment to evaluate founders and problems as an integrated whole.

That’s the core reason SVTR continues to build its AI venture ecosystem.

What SVTR aims to document isn’t a collection of AI founder résumés, but a series of founder × problem × product form combinations.

Our AI venture database doesn’t just track founder backgrounds — it tracks the problems companies are tackling, product evolution, funding progress, competitive positioning, and capital relationships.

Our AI venture commentary doesn’t just chase headlines. It tries to answer: Why does this problem matter right now? Why might this company become a new variable? Why is the capital market repricing this direction?

And our AI venture events and programs aren’t about putting founders and investors in the same room. They’re about making sure that people with genuine problem judgment, product judgment, and industry insight get seen earlier and connected more precisely.

Going forward, we want it to be more than a database. We want it to be a signal source for AI investing:

Helping founders get discovered by the right capital and industry partners.

Helping investors identify teams with real problem judgment earlier.

Helping industry players systematically understand AI startups’ technology, product, and commercialization positions.

We believe the next truly important AI companies may not emerge from the most glittering résumé lists. They’re more likely to come from people who are already seriously defining problems, seriously building products, and seriously navigating real markets. What we want to do is make those signals visible — sooner.