Top-tier VC partners are stepping in collectively to bet on the "mundane backend" of vertical Agents | SVTR Signal

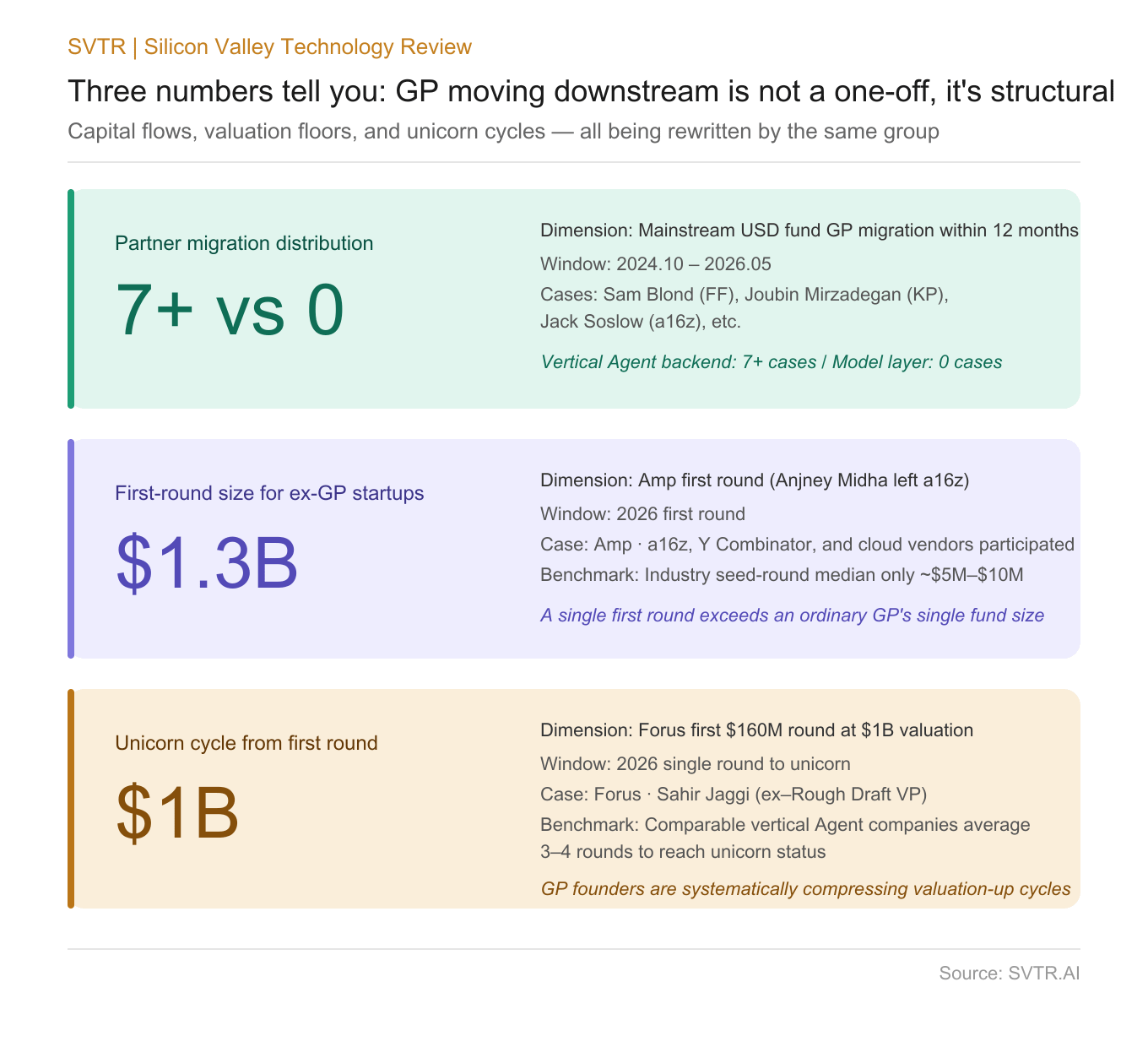

The real signal last week is not another vertical Agent financing reaching unicorn status, but the fact that over the past 12 months, at least seven current or former partners of mainstream US dollar funds have shifted from buy-side to sell-side roles, with their investment tracks highly concentrated on enterprise back-end sectors.

SVTR believes this is one of the most underrated secondary signals of 2026. A group of elites with the most solid information advantages are voting with their feet to redefine the real moat of the vertical Agent track. It lies neither in models nor data, but in category insights and go-to-market strategies. The homogenization at the model level has driven the marginal value of merely understanding technology down to nearly zero. Meanwhile, the genuine barriers of vertical Agents happen to fall within the core strengths of these VC partners.

It is noteworthy that such career shifts have not taken place in seemingly grander fields such as model development, foundational AI enterprises or chip sectors. Even the most high-profile tracks have failed to attract partners to step into actual business operations. As the window for information arbitrage on deal sourcing narrows, they opt to participate in the industry in person rather than making more aggressive investments.

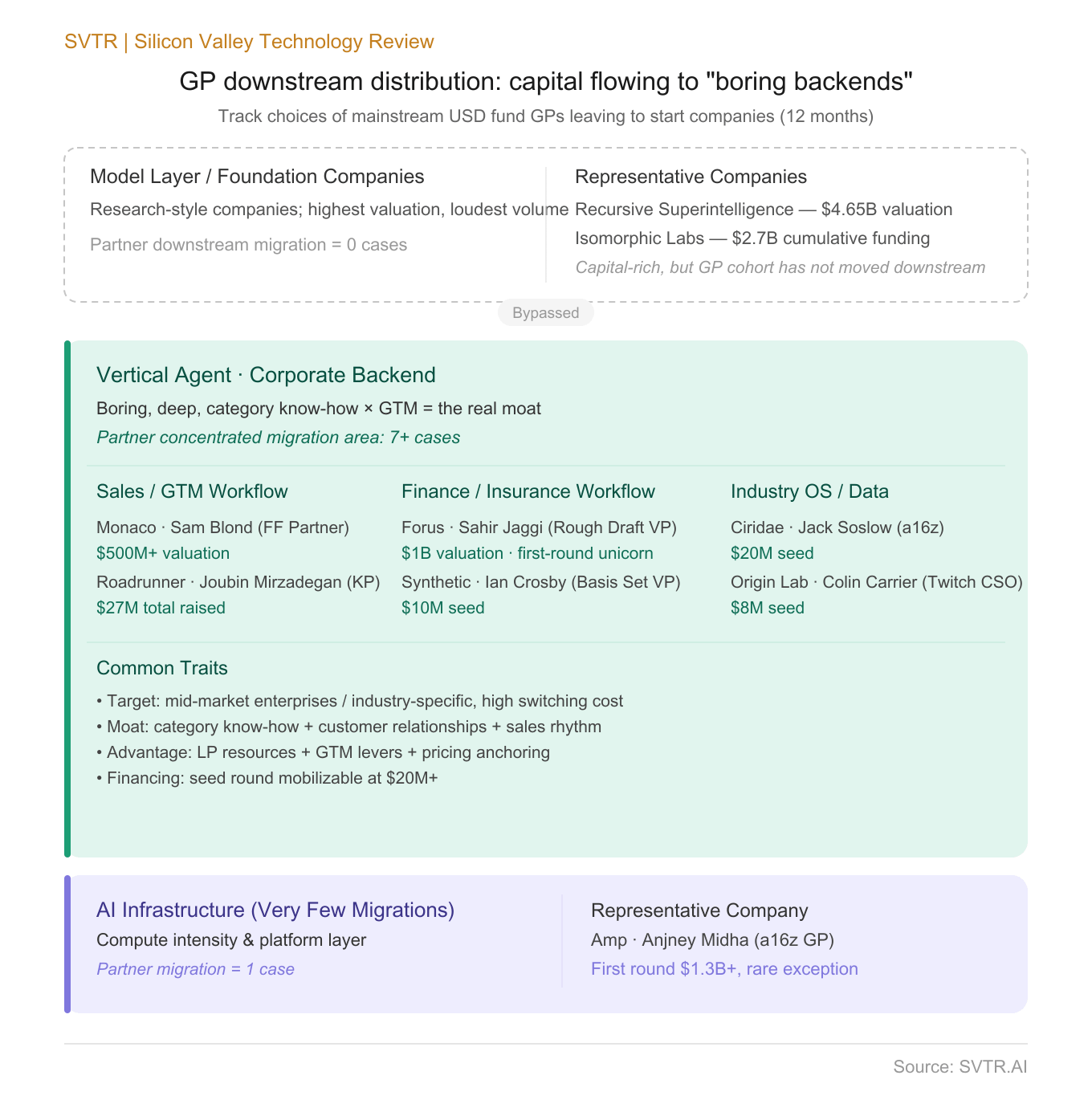

Signal 1 | Partner migration is highly concentrated in the "enterprise back-end"

Over the past 12 months, there have been at least seven clearly documented cases where partners from mainstream US dollar funds left their positions to start their own businesses:

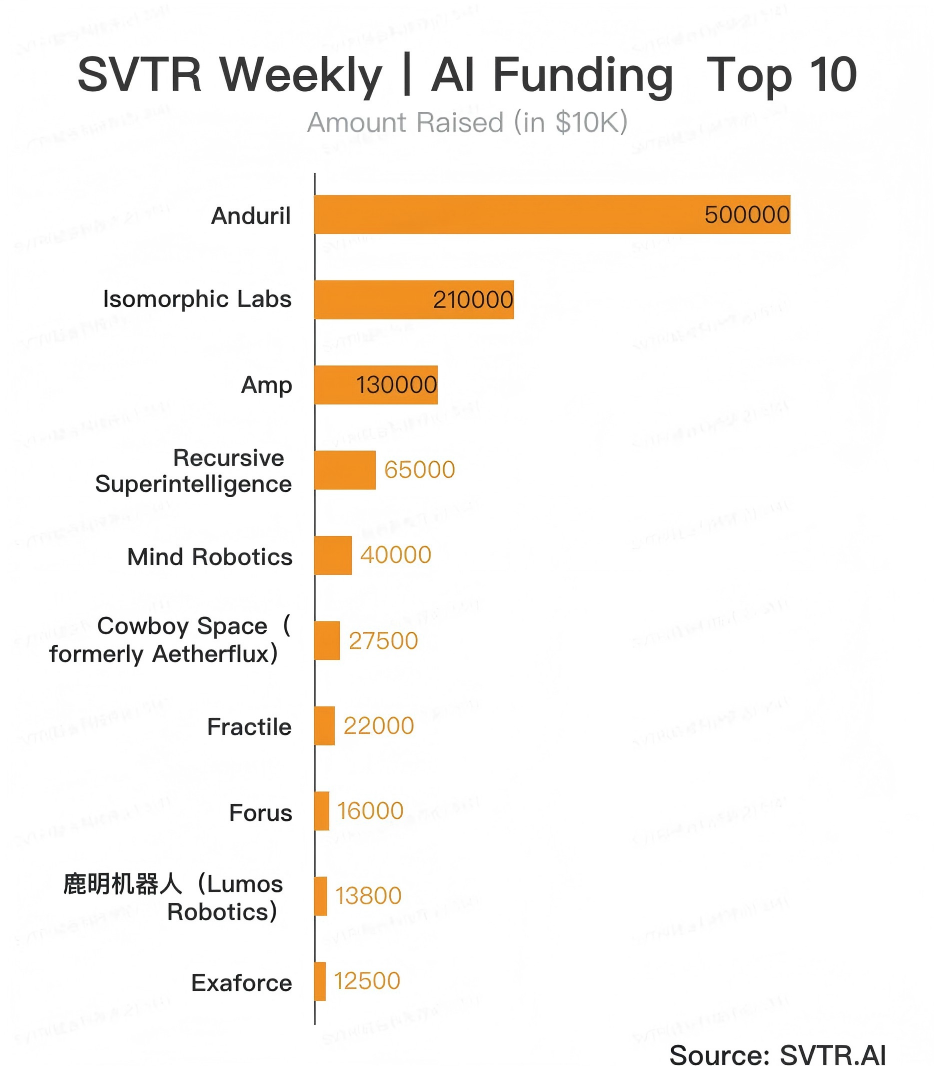

a16z GP Anjney Midha → Amp: AI compute tuning, first-round raise exceeding 130M

Kleiner Perkins GP Joublin Mirzadegan → Roadrunner: AI-native CPQ, with a total funding of 27 million US dollars raised through seed and Series A funding

a16z Partner Jack Soslow → Ciridae: an AI operation system for mid-sized enterprises, which secured $20 million in seed funding

Founders Fund Partner Sam Blond → Monaco: an AI sales platform, which raised $50 million in Series B funding with a valuation exceeding $500 million

Basis Set Venture Partner Ian Crosby → Synthetic: an AI accounting firm, which obtained $10 million in seed funding

Rough Draft VP Sahir Jaggi → Forus: an AI prescription and insurance process platform, which closed a $160 million initial round and became a unicorn enterprise

Twitchex CSO, angel investor with investments in over 50 companies ColinCarrier → OriginLab: a provider of world model training data, which raised $8 million in seed funding.

If we broaden the scope to include senior investors and serial entrepreneurs, and further add Cowboy Space co-founded by Baiju Bhatt, co-founder of Robinhood (raised $275 million in Series B funding with a valuation of $2 billion), Exponent founded by Charlie Cheever, co-founder of Quora, and Recursive Superintelligence led by Richard Socher, former Chief Scientist of Salesforce (post-money valuation of $4.65 billion), the figures will rise even higher.

What makes this list counterintuitive is not the fact that these people have left their previous positions, but that they have collectively steered clear of the most high-profile tracks such as large models, chips and consumer-oriented AI.

Signal 2 | Not Betting on Technology, But on “GTM × Category Insight”

Analyzing what these companies are offering: CPQ solutions, accounting bookkeeping, sales compensation management, prescription pricing, franchisee financial management, insurance brokerage services, sales process management and more. Almost all of them are enterprise back-end businesses that are mundane yet deeply accumulated, entail high switching costs and require mastery of industry-specific terminology. The real barriers to entry in these sectors have never lain in model selection, but in the tripartite combination of industry expertise, client relationships and sales rhythm control.

What core strengths do VC partners possess? They have built up insights into customer profiling, sales rhythm mastery and valuation benchmarking by evaluating 2,000 companies over a decade. These are precisely the most scarce resources for vertical Agent companies in their rapid expansion phase. The biggest bottleneck for founders of vertical Agent enterprises is usually not how to train Agents, but how to get involved in procurement negotiations, set reasonable pricing benchmarks and secure the first batch of reference clients. Former general partners hold inherent structural advantages in these three aspects.

In other words, they did not enter the industry merely drawn by the AI boom; instead, they realized their inherent strengths could for the first time be monetized on the seller side. If such core strengths can be revalued, what changes will take place across the entire VC value chain?

Signal 3 | The Sourcing Era Is Ending; The Underwriting Era Is Just Beginning

This is truly a third-tier pivotal signal. If the optimal strategy of frontline GPs has shifted from “finding the next Forus” to “establishing the next Forus independently”, the value chain of the VC industry is being rewritten.

Over the past five years, excess returns from AI investments mainly stemmed from sourcing advantages — being the first to spot OpenAI, Anthropic, or issue term sheets to Cursor. However, vertical Agent projects are overly saturated and fragmented, and the technical gaps are too narrow for GPs to maintain prominent sourcing edges. The likelihood of five high-caliber AI Sales Agent startup teams emerging simultaneously is far higher than that of five equally strong foundational AI company teams.

As information arbitrage opportunities in sourcing fade away, excess returns will flow back to two types of participants: funds equipped with industrial know-how to conduct professional underwriting, and partners with GTM leverage capable of launching startups on their own. The logical closed loop behind this trend is fully formed. The only remaining question is: why did this trend break out intensively between 2025 and 2026, rather than in 2023 or 2024?

Causes | Why Now?

Three major forces are taking effect simultaneously:

Technological inflection point. The marginal capability gaps at the model level are narrowing to zero, forcing vertical Agents to shift their competitive moat toward go-to-market strategies and category insights. In 2024, startups could still secure Series A funding by claiming “superior Agent orchestration technology”, yet this growth narrative has lost its appeal by 2026.

LP inflection point. Starting from Q3 2025, dollar limited partners have grown far less patient with reinvesting in foundational AI companies, and capital is flowing toward application-layer ventures with proven revenue streams and verifiable unit economics. Leading general partners can directly sense this shift in sentiment during LPAC meetings, at least six months earlier than such trends appear in secondary research reports.

Incentive inflection point. The carry profit realization timeline of top-tier GPs is no longer aligned with the market opportunity windows they identify. If a GP forecasts a seed-stage project they would traditionally back could surge tenfold in value within five years, while carry profits locked in the fund take eight years to vest and get split among a 20-person core team, the expected returns from personal direct investments outpace long-term career gains within institutional funds.

This checklist comes into being precisely as these three inflection points converge.

Impact | Who Gets Hit

Founders: The profile of real competitors has shifted. Over the past 18 months, vertical Agent entrepreneurs have mainly faced competition from peer founders and incumbent software companies. Going forward, this competitive landscape will welcome a new group of “ex-GP founders” who come equipped with limited partners (LPs), go-to-market (GTM) networks, client rosters and secondary valuation benchmarks. Their edge lies not in products, but in pre-established financing rhythms and sales networks. They can mobilize over 20 million US dollars at the seed round stage, and skip traditional demos to directly connect with strategic LPs in Series A financing. Ordinary founders need to rethink their differentiated positioning: superior technology is no longer sufficient. They must prove they possess irreplicable industrial expertise in specific niche sectors that even GPs cannot match, such as exclusive client connections, unique data flywheels, or hard-to-replicate founder-market fit within the industry. A concrete strategic takeaway is that instead of pursuing general horizontal Agents, it is wiser to firmly anchor the business in vertical industries overlooked by GPs.

Investors: The era of deal-sourcing arbitrage is drawing to an end. A clear inference is that if even firm partners are launching their own startups, the scarcity of merely discovering investment deals will inevitably decline, while the scarcity of accurately evaluating projects will rise sharply. The moat of early-stage funds is shifting from gaining early access to projects to identifying industry ceiling potentials ahead of others. This means capabilities once regarded as cost centers, including investment research teams, industry analysts and exit return models, are becoming core factors in investment valuation. Meanwhile, the transferable value of secondary valuation benchmarks and LP connections is growing increasingly prominent, and early-stage personal connections alone can no longer sustain the differentiated competitiveness of new funds. Mid-sized funds need to stay highly vigilant; under this new supply-side logic, funds that are neither large enough to provide underwriting support nor close enough to participate directly in industrial layout are in the most precarious position.

Platforms and Major Enterprises: These vertical Agent enterprises pose the most direct substitution threat to SaaS giants including Salesforce, ServiceNow and Workday within the next 24 months, and merger and acquisition activities are expected to surge notably starting from the second half of 2026.

Enterprise Clients: CIOs and CFOs are no longer faced with the simple choice of whether to adopt AI tools. Instead, they have to decide between purchasing AI modules developed by established incumbents or brand-new AI-native platforms built from scratch. The latter have already accumulated client cases with annual recurring revenue (ARR) ranging from 600,000 to 1 million US dollars.

Verification: Three Key Indicators Worth Tracking

Within 90 days, check if more than two current partners from a16z, Founders Fund, Kleiner Perkins and Sequoia resign to start their own businesses, with their business focus still centered on enterprise backend Agents. If this happens, it indicates a structural industry shift rather than isolated individual cases.

Verify whether the median post-money valuation of seed-stage vertical Agent enterprises exceeds 50 million US dollars before Q3 2026. This is a core threshold to judge whether general partners are systematically lifting the bottom valuation of this track.

Confirm if there emerges the first public case of seed financing initiated by former GPs with participation from their former venture capital funds within 90 days. This will officially signal the recognition of this new supply-side logic by limited partner capital.