The Real Competitor for AI Agent Companies Is the Payroll, Not SaaS Budgets | SVTR Signal

SVTR observes that AI agent B2B subscription businesses are systematically decoupling from the SaaS track. They still look like “services for businesses drawing corporate budgets,” but the decision-maker profile and growth curve have already left the software spending lane entirely. Their strategic competitor is the corporate payroll, not other SaaS products.

Continuing to evaluate agent companies with standard SaaS metrics — LTV/CAC, net retention rate, 120% expansion rate — will systematically underestimate their growth ceiling: global enterprise IT budgets sit at roughly $500 billion; human-related spending (wages, professional services, outsourcing, recruitment costs) is more than ten times that. The underlying AI infrastructure layer is a separate discussion beyond this issue’s scope.

Signal 1 | Professional Domain ARR Growth Already Differs by Order of Magnitude from SaaS

Several data points observable over the past month:

Contrario, a YC W25 AI recruiting company, reached $6M ARR in under 6 months on a seed round of just $2.3M

Viktor, an AI coworker embedded in Slack and Microsoft Teams, hit $15M annualized revenue in 10 weeks, raising a $75M Series A

Searchable, an AI search visibility platform for brands, reached $2M ARR in a few months

Vétir, an AI outfit selection and wardrobe management app, disclosed 3,500% B2B customer growth and 9x annual revenue

Benchmark: Traditional SaaS companies take a median of 3–5 years to go from zero to $10M ARR. These AI agent companies did it in months.

The difference isn’t product quality — it’s who’s making the buying decision. Contrario’s buyer isn’t the CIO; it’s the HR director. Viktor’s buyer isn’t IT ops; it’s the business team lead. When an HR director is calculating “can this tool save me the cost of a $120K/year recruiting manager,” the decision logic is no longer software procurement — it’s labor substitution. The former has a small budget pool and slow decisions; the latter has a large budget pool and fast decisions.

This leads to the more important question: What exactly are investors pricing in right now?

Signal 2 | Capital Is Systematically Valuing “Professional Services Substitutes”

Reorganizing mid-to-late-stage financings from the past month by the function being replaced:

Legal: Stilta ($10.5M seed, a16z + YC, AI patent analysis), Lexroom ($50M Series B, European civil law AI law firm operations), LawX ($8.7M seed, AI legal case sourcing system)

HR / Recruiting: Contrario ($2.3M seed, $6M ARR in 6 months)

Wealth & Asset Management: Farther ($150M Series D, unicorn status, AUM exceeds $ 23B), Moment ($78M Series C, AUM exceeds $ 10tn)

Medical Administration & RCM: Commure ($70M raise, $7B valuation)

Email Security & Enterprise Communications: Ocean ($28M raise, processing over 1 billion emails monthly), Tribal ($10M seed, agents on Salesforce)

These companies boast high valuations when measured by SaaS metrics. However, if we adopt a different benchmark — the total global payroll for the professional roles being replaced — their valuations actually appear conservative. Farther targets the service fee income of global wealth advisors; Lexroom cuts down the billable hours spent on legal research by European law firms; Commure reduces the labor costs of entire teams responsible for revenue cycle management in hospitals.

One detail worth noting: Farther has completed its Series D round, Lexroom its Series B, and Stilta its seed round. Yet their valuation-to-ARR ratios have converged. This indicates that investors believe this track boasts a high success rate and clear exit prospects, so they are willing to offer late-stage valuations for early-stage companies. This represents a capital trajectory entirely different from that of SaaS businesses.

So are the moats of traditional SaaS (product complexity, integration depth, ecosystem dependency) still important? The answer lies in the profiles of the founders.

Signal 3 | Founder Profiles Have Shifted from “SaaS Serial Entrepreneurs” to “Core AI Engineering + Domain Expertise in Parallel”

Representative founder backgrounds from recent financings:

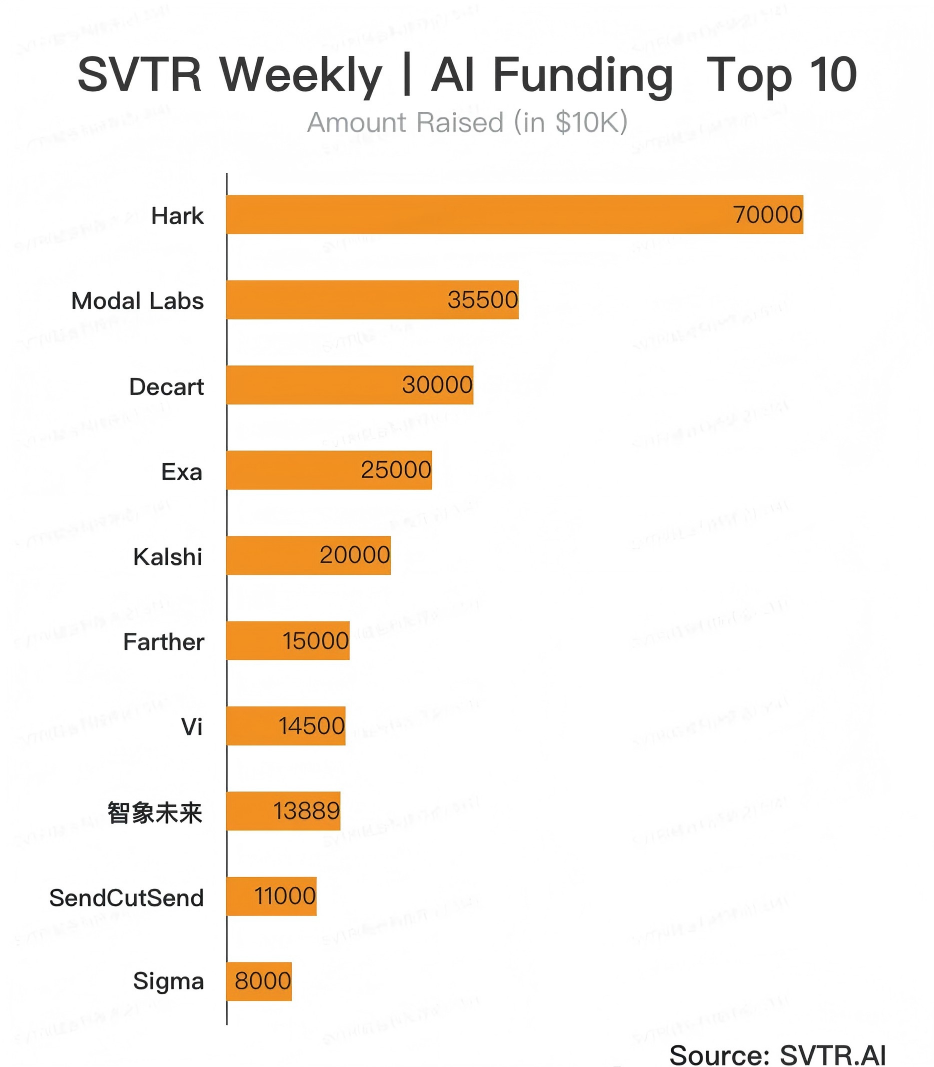

Hark: Brett Adcock, current CEO of Figure; serial entrepreneur (Vettery acquired by Adecco, Archer went public). New company raised $700M Series A at $6B valuation

Decart: Dean Leytensdorf, Israeli 8200 military intelligence unit; earned a Technion CS PhD at 23. $300M raised, ~$4B valuation

Unframe: Shay Levi, co-founder of Noname Security (acquired by Akamai for $450M), second-time founder

IrisGo: Jeffrey Lai, former Apple Siri engineering manager, incubated by Andrew Ng’s AI Fund

Modal Labs: Erik Bernhansson, former CTO of Better.com, former engineering manager at Spotify

Catena Labs: Sean Neville, co-founder of Circle

These founders share one trait: they aren’t people who “know SaaS GTM” — they’re people who “understand core AI capabilities + have judgment in a specific professional domain.” Investors can complete due diligence faster; the resume accounts for half of the process. Early-stage valuations in the agent space are driven up by founder scarcity, not product/revenue metrics. This in itself is a fork in the road from typical SaaS investment logic.

Cause | Why Now

Three variables converged simultaneously from late 2024 to mid-2026, creating the current market:

1. Technology matured. LLMs crossed the reliability threshold for independently completing professional tasks. Repeatable work — legal research, recruiting screening, wealth advisor queries — now has stable product forms.

2. Budget shifted. Beyond enterprise IT budgets, the “human labor budgets” of HR, operations, legal, and finance departments are now formally part of AI procurement discussions. The decision-makers for this budget pool are not in IT — they’re on the front lines of business.

3. Distribution matured. Salesforce, Slack, and Microsoft 365 have opened up agent integration channels. Agent products no longer need to build their own sales and distribution paths — they can embed into existing enterprise entry points. Distribution factors now outweigh product in weighting. For example, Viktor’s ability to reach $15M ARR in 10 weeks owes far more to distribution than to product.

These three things had each happened individually before. Their simultaneous occurrence is what constitutes a brand-new market structure.

Impact | Who Gets Affected

Entrepreneurs: The window for vertical professional domains is shorter than commonly assumed. Don’t build generalized “agent platforms” — beware of being directly displaced. If entering a horizontal track, don’t build a general platform; be the #1 in a vertical domain, owning one function or one job type. The key shift is pricing from “per seat” to “per labor hour / task saved.” Building a general-purpose agent platform has high failure probability, because agents are more scenario-specific and fragmented than SaaS, and the channel economics above them are already forming. One contrarian view: model capability is not the biggest moat — “being able to clearly calculate how many labor hours I save clients each month” is what determines whether you win. Customers will pay a premium for quantifiable human cost savings.

Investors: The valuation anchor needs to change. LTV/CAC still matters, but the ceiling should shift from “this SaaS sub-sector market share” to “total global wage expenditures of the corresponding function.” The core of net retention should shift from “seat expansion rate” to “labor substitution growth rate“ — customer stickiness is no longer a pleasant surprise; what matters is human market share for that function. Agent company return cycles will compress from SaaS’s 7–10 years to 5–7 years, as valuation jumps happen faster and both PE takeover and strategic acquisition exit paths open simultaneously. Early ARR should also be re-framed around “payroll substitution”: customers care more about how much you save them. As long as agent task reliability exceeds what’s promised, retention cycles will be shorter than SaaS but customer expansion will be higher.

Big Platforms: Salesforce, Microsoft, Slack — companies with workflow entry points — are acquiring new strategic leverage. The rules they set for who gets agent channel access will themselves become the source of the next generation of take rates.

Enterprise Buyers: The budget boundary between CIO and CHRO/CFO is beginning to blur. A hybrid procurement committee will emerge in the next 12 months.

Validation: Three Key Metrics to Track

Within 90 days: Track whether representative companies like Contrario, Viktor, and Stilta continue maintaining ARR growth exceeding 5x annualized rate. Regression to the SaaS median (2–3x) would mean the “payroll substitution” narrative has been over-discounted by the market.

Within 90 days: Watch for whether any agent company formally writes a “percentage share of saved labor budget” clause into contracts. This is hard evidence that the labor-hour billing model is formally accepted — and will trigger enterprise finance-side accounting classification changes.

Within 90 days: Watch whether Salesforce or Microsoft launches a clear take-rate mechanism for agent integration (like an App Store model). Once established, channel economics will rapidly reshape early-stage valuations. Horizontal agent companies bound to major platforms will see their valuations surge first.