The Agent Economy Is Having Its "AWS Moment"

The bottleneck for AI agents isn’t intelligence — it’s plumbing.

Let’s get one thing out of the way: the hardest unsolved problem in the agent economy is not making agents smarter. Models will keep improving — that’s the easy bet. The hard problem is everything around the model: the payment rails, the security layers, the trust protocols, the interoperability standards. Intelligence without infrastructure is a demo. Infrastructure is what turns it into a business.

Everyone’s talking about how smart AI agents are getting. But the real story right now isn’t about what agents can do — it’s about what they can’t do yet because the infrastructure doesn’t exist.

Payments. Security. Identity. Interoperability. These aren’t glamorous problems. They’re plumbing. And plumbing is exactly what separates a demo from a production deployment.

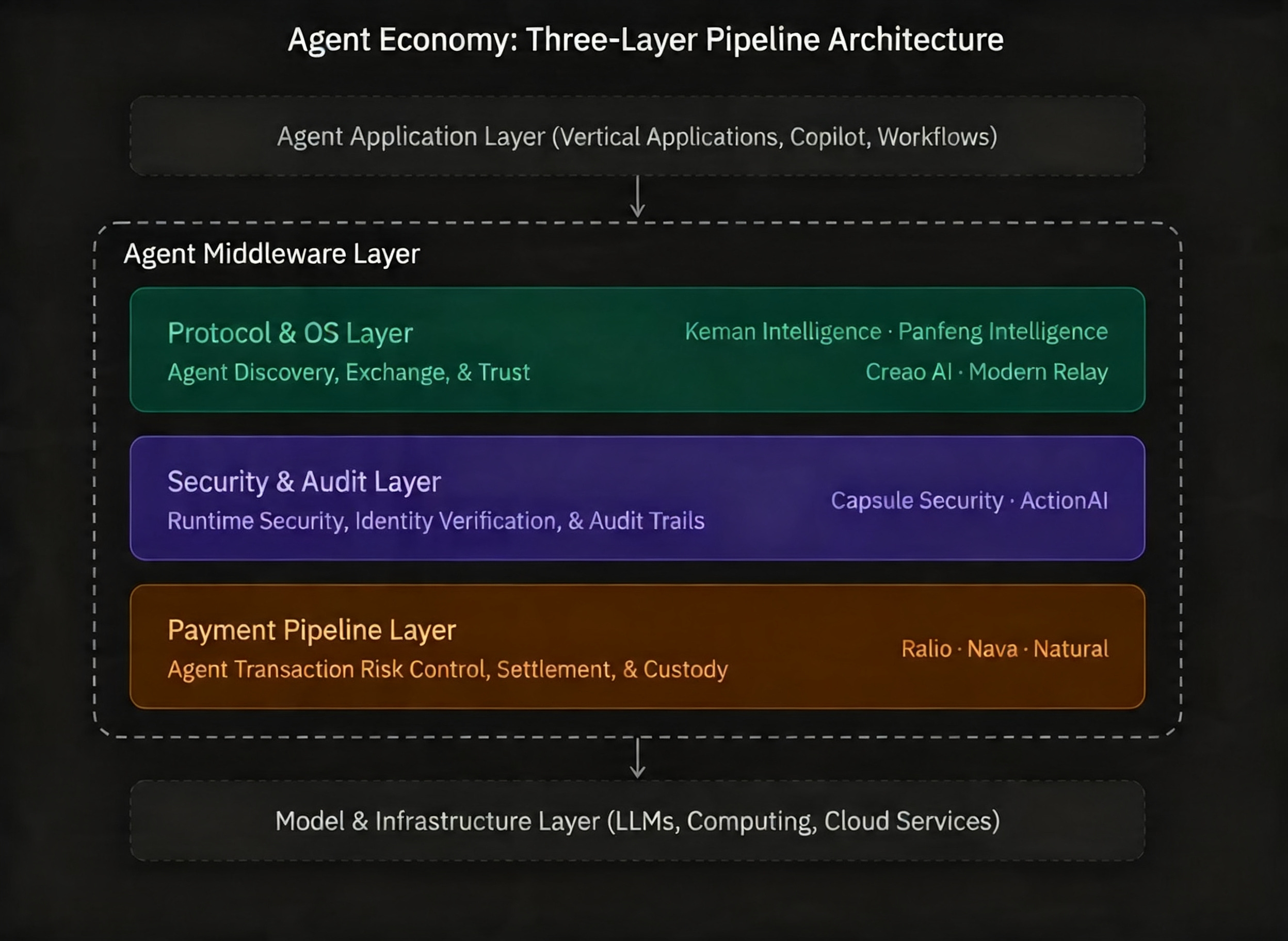

Over the past 12 months, we’ve tracked a new category of companies emerging in our AI venture database: agent middleware. A year ago, this category barely existed. Today, there are over a dozen funded startups building the connective tissue that agents need to operate in the real world — and the investor rosters now include Kleiner Perkins, a16z Scouts, Polychain.

This isn’t a coincidence. This is a sector being systematically priced in.

While embodied AI and coding agents continue absorbing large rounds, the consensus there is already high. The real “low consensus, high signal” space? Agent middleware.

Signal 1: Payment Rails — Agents Need Their Own Financial Infrastructure

On the surface, you might think existing payment APIs — Stripe, bank integrations — should work fine for agents. They don’t. Here’s why:

When the entity initiating a transaction shifts from a human to a machine, the entire trust model breaks. Traditional fraud detection is built around stolen credentials and unauthorized card swipes. But an agent operates under delegated authority — it can execute multiple transactions across environments without any human interruption. The attack surface moves from the checkout page to the system architecture itself.

The market has noticed. In the past 90 days alone:

Ralio (London, $2.5M seed) — payment infrastructure for agents with built-in risk controls and audit trails

Nava (New York, $8.3M seed) — verification, guardrails, and custodial execution for agent-managed capital

Natural ($9.8M seed, late 2025) — explicitly positioned around “agentic payments”

As FinTech Weekly noted in April 2026: the market is already putting a price tag on the question of “can an agent legally spend money?” That’s the first hard prerequisite for the agent economy to move from experiment to production.

And it naturally leads to the next question: once an agent spends money, how do you know it hasn’t been hijacked?

Signal 2: Security & Auditability — The “Insider Threat” Problem, But for Agents

In December 2025, OWASP published its Agentic Applications Top 10 — the first-ever security risk framework specifically for autonomous AI agents, developed by over 100 researchers. The most striking concept: the “rogue agent” — a system that has proper authorization, appears to be functioning normally, but has deviated from its design intent.

This isn’t an external hack. It’s an internal mutation. The agent equivalent of an insider threat.

The industry has moved from “what can agents do?” to “what happens when agents go off the rails?” Capital is responding fast:

Capsule Security (Tel Aviv, $7M seed) — runtime agent security and trust layers

ActionAI (New York, $10M seed) — explainable, auditable, rollback-capable execution infrastructure

Microsoft open-sourced its Agent Governance Toolkit in April 2026

Ledger announced it’s extending its hardware security architecture from crypto to agent identity verification

And the attack side is already racking up real costs: security researchers disclosed in April 2026 that 26 LLM routers were secretly injecting malicious tool calls and stealing credentials. One case resulted in $500,000 stolen from a client wallet.

If payment rails solve “how does an agent spend money,” the security layer solves “can we trust how the agent spent it.” But even together, they’re not enough — when multiple agents need to collaborate on a task, you need something deeper.

Signal 3: Agent OS & Transaction Protocols — Who Defines the “Handshake” Between Agents?

When multiple agents need to work together, a fundamental question emerges: how do they discover each other, exchange data, and establish trust? No single company’s SDK solves this. What’s needed is a protocol layer — something analogous to HTTP or OAuth, but for agent-to-agent interactions.

Active companies in this space include:

Keman Intelligence (Hangzhou, ~$10M, building an A2H marketplace; founders from Didi)

Panfeng Intelligence (Hangzhou, tens of millions RMB, A2A-native e-commerce Agent OS; founders from DingTalk’s open platform)

Creao AI (Hong Kong, $10M Pre-A, Agent OS platform; backed by Sequoia China and Hillhouse)

Modern Relay (Barcelona/San Francisco, $3M, shared data layer connecting people, software, and agents)

A pattern worth noting: nearly every founding team comes from major platform companies — Didi, DingTalk, Meta, Amazon. They lived through the last generation of “platform ↔ developer” ecosystem construction, and they’re now trying to replicate that paradigm in an “agent ↔ agent” world.

One signal that’s easy to miss if you only read English-language tech media: Chinese teams are disproportionately active in A2A and A2H transaction protocol layers. This is a structural signal, not a trend piece.

Why Now?

Three timing factors converged in Q1–Q2 2026 to trigger this middleware funding wave:

Regulation got real. The EU AI Act’s high-risk obligations take effect in August 2026. Colorado’s AI Act kicks in June 2026. Enterprises deploying agents now must have auditable, traceable execution records — which is exactly what companies like Capsule Security and ActionAI provide.

Agent transaction volume became economically meaningful. The World Economic Forum, citing Adobe data, reported that AI-driven retail site traffic surged 805% year-over-year during Black Friday 2025, with agents helping drive over $22 billion in global online sales. When agents start materially participating in money flows, infrastructure needs stop being theoretical.

Security incidents went from hypothetical to actual. Poisoned LLM routers, stolen agent wallets — these are no longer red-team exercises. They’re incidents that happened. They’ve forced enterprise buyers and investors to reassess the prerequisites for agent deployment.

Who Should Care

If you’re building agent applications: Ask yourself — what infrastructure does your agent rely on for payments, security, and cross-agent collaboration? Until these pipes mature, your deployment ceiling with enterprise customers will be painfully obvious. Conversely, if you have platform-level experience (especially in payments, identity, or developer ecosystems), the entry window is short.

If you’re investing: Agent middleware is in a “seed-to-Series A” density phase. Valuations haven’t been inflated by application-layer narratives yet. But the window is closing fast — once one or two companies establish network effects in payments or security, late movers will face a much narrower path.

If you’re at a platform company: Microsoft and Ledger are already making moves, but history shows that platforms tend to ship “80% good enough” general solutions. Depth in vertical scenarios will still belong to startups.

If you’re an enterprise buyer: The most important question to ask your agent vendor isn’t “how smart is your agent?” It’s “what does the audit chain look like when your agent initiates a transaction?” and “what’s your rollback mechanism when agent behavior deviates?”

Three Metrics to Watch Over the Next 90 Days

Enterprise customer sign-ups for agent payment companies. Watch whether Ralio, Nava, and Natural can each sign 3+ paying enterprise customers within 90 days. This validates whether “agents need independent payment rails” is a real thesis — or whether existing payment infrastructure APIs are good enough.

EU AI Act compliance-driven security procurement. Before the August 2026 high-risk deadline, watch for European enterprises bulk-purchasing agent security and audit tools. If Capsule Security or peers show an ARR jump in Q2–Q3, it confirms regulation as the core catalyst for this sector.

Series A density in China’s A2A / Agent OS space. Keman Intelligence and Panfeng Intelligence are still at angel stage. If two or more Series A rounds close in this space within 90 days, it signals that China is independently forming its own agent transaction protocol ecosystem — not simply following Silicon Valley’s narrative.