OpenAI Secretly Files S-1: Racing to IPO Window After Being Overtaken by Anthropic on ARR

On May 22, 2026, OpenAI filed a confidential draft S-1 for an initial public offering with the U.S. SEC, with Goldman Sachs and Morgan Stanley as underwriters. The target listing window is September to November this year, with a target valuation of no less than $1 trillion. The current private market valuation stands at $852 billion (post-money), backed by cumulative financing of $122 billion.

The timing of the filing was not coincidental: on May 18, a California federal jury dismissed all of Elon Musk’s claims against OpenAI, clearing the most critical legal obstacle in the IPO process. In September, CFO Sarah Friar favored a longer preparation timeline. The current filing reflects CEO Sam Altman’s push for a September listing, with the CEO’s position prevailing over internal disagreements on pacing.

The article argues that the real signal of this filing is not the label of “world’s largest AI IPO”, but rather that OpenAI chose to proactively lock in public market pricing power and narrative control at the moment when the three battlegrounds — ARR growth rate, operational profitability, and valuation multiples — are about to fully diverge from Anthropic. This is a defensive preemption, not a winner’s posture.

I. ARR Growth and Valuation Multiples Have Already Reversed

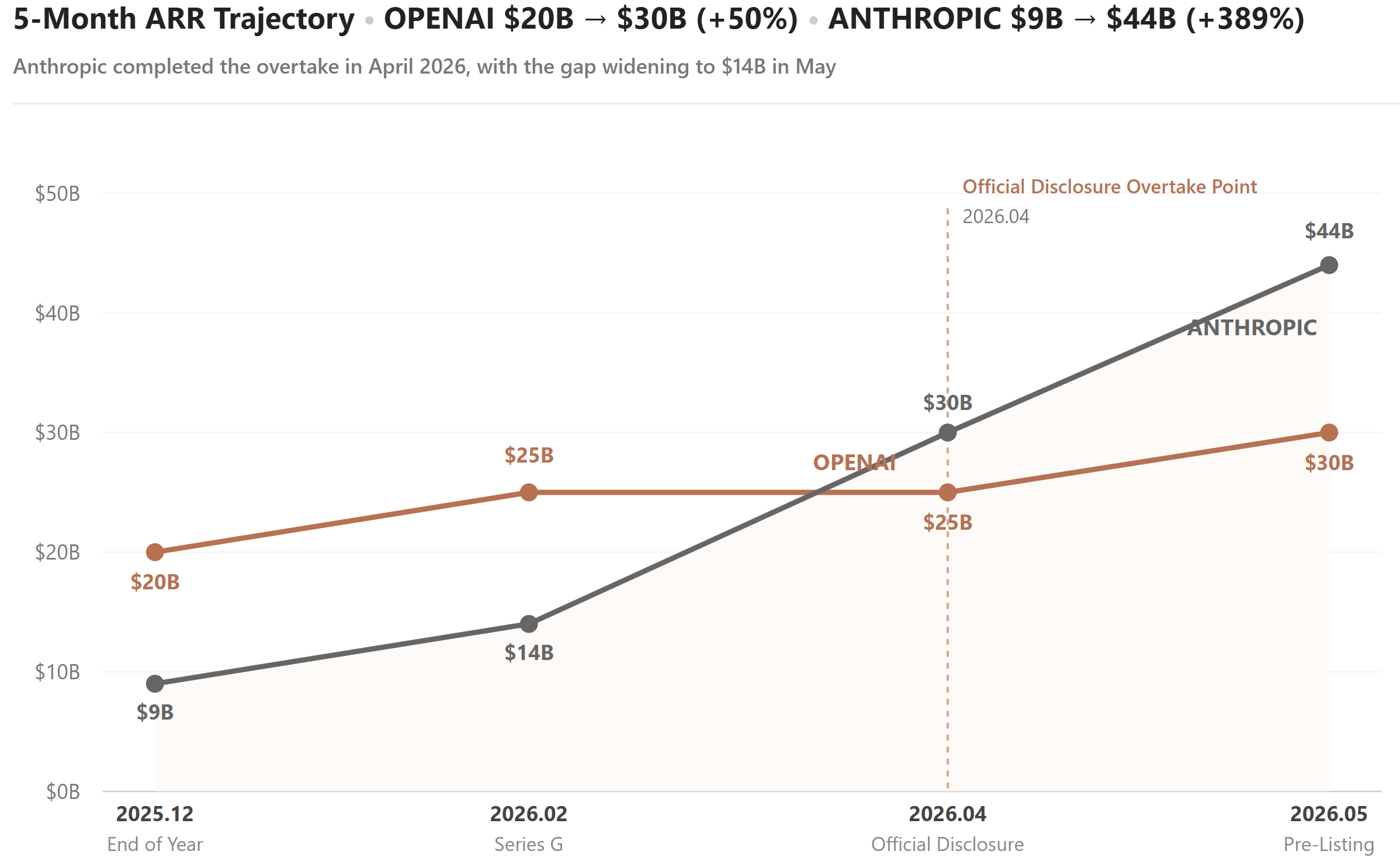

When the annualized revenue trajectories of both leading companies are plotted together, the reversal inflection point appears in Q1 2026:

OpenAI rose from $20 billion ARR at end-2025 to approximately $24 billion by April — ~25% growth in 5 months;

Anthropic surged from $9 billion to $30 billion (official disclosure) over the same period, and according to follow-up reports from The Information and SemiAnalysis, the run rate was approaching $44 billion by May.

OpenAI Q1 actual revenue was $5.7 billion; Anthropic Q1 was $4.7 billion — the gap narrowing to a $1 billion range.

Valuation multiples calculated on current disclosed bases:

OpenAI: $852B / $24B ARR ≈ 35x

Anthropic: $380B / $14B ARR ≈ 27x in February funding round negotiations; $900B / $44B ARR ≈ 20.5x in this month’s new negotiations

The implied secondary market pricing for Anthropic has also touched $1 trillion. As Anthropic overtakes on ARR, valuation multiples are converging — meaning OpenAI can no longer sustain a 35–40x ARR multiple on the basis of “industry leader” scarcity premium. This is the direct trigger for the preemptive filing.

II. Is the $1 Trillion Anchor Sustainable?

Bull case for $1 trillion target valuation has three pillars:

Private valuation trajectory rising consistently for 12 months: ~$157B at end-2024 → ~$500B in October 2025 → $852B this round;

Microsoft remains both largest customer and largest compute provider — the partnership framework provides a capital markets narrative of locked-in revenue streams;

Dual consumer and enterprise lines — business structure is broader than API-only Anthropic.

Bear case data is equally clear:

Absolute growth has been overtaken: Anthropic grew ARR 4.9x in 5 months; OpenAI only 1.25x over the same period. Even at a 40x ARR target, OpenAI’s pricing is less justified than Anthropic’s current implied 20–22x multiple;

Operational leverage is moving in opposite directions: Anthropic may achieve its first operational profit in Q2; OpenAI’s losses are widening over the same period. CFO Friar — bound by a 5-year, $600 billion compute commitment — has publicly acknowledged that revenue growth is insufficient to support all data center construction. This is an unavoidable risk exposure in the S-1 roadshow;

Governance terms unresolved + banker conflicts: Revenue sharing with Microsoft, IP ownership, and board power dynamics are not fully publicly disclosed. The underwriting syndicate of Goldman Sachs and Morgan Stanley are simultaneously in talks with Anthropic about its IPO. The same roadshow team must pitch two direct competitors to the same pool of LPs — this is yet another motivation for OpenAI to file first.

III. Transmission to the financing environment of the track

OpenAI’s filing will squeeze competitors on two levels:

1. Infrastructure comparable anchor reset

GPU cloud and training platforms like CoreWeave, Lambda Labs, and Together AI — once detailed OpenAI compute expenditure data becomes available as a benchmark — will face recalibration of their current 9–15x revenue multiples in private market pricing. Some companies may be forced to prematurely disclose take-or-pay contract details.

2. Window compression effect

SpaceX publicly filed its S-1 on May 20 (target valuation $1.75 trillion, raising $75 billion, Nasdaq ticker SPCX), with a roadshow scheduled to launch June 5 and pricing around June 12. OpenAI confirmed its filing just two days after SpaceX’s S-1 went public — the time-window pressure is immediate. Q3–Q4 will see at least $150 billion combined in mega-issuances from SpaceX and OpenAI. The listing window for mid-tier AI companies is effectively pushed to Q1 2027 or later.

For Anthropic, however, OpenAI’s filing timing actually presents a tactical opportunity: its proposed $900 billion private round can be completed before OpenAI’s public S-1, positioning Anthropic as the “unlisted but ARR- and profit-stronger” comparable before its own roadshow.

IV. Three Variables to Watch Over the Next 1–2 Quarters

1. OpenAI’s public S-1 disclosure — gross margin and Microsoft revenue-sharing mechanism

The public S-1 is expected 15 days after the confidential filing, i.e., no earlier than mid-to-late August. Key metrics to watch: if gross margin is significantly below secondary market implied assumptions, or if the Microsoft revenue-sharing mechanism is above market-estimated take rates (~20% range), the $1 trillion valuation will likely fall back to the $750B–$850B range.

2. Whether Anthropic files before OpenAI’s public S-1, and its disclosed Q2 operating profit data

If Anthropic files and can demonstrate Q2 profitability, OpenAI will face the “industry leader” narrative being dismantled. OpenAI’s valuation would face substantive downside, with the lower bound potentially breaking through $700 billion.

3. SpaceX’s June offering results and final pricing range

SpaceX’s current target is $1.75 trillion at $75 billion raise. If the final issuance valuation falls below $1.5 trillion, or the price drops to the lower end of the issuance range within 30 days after pricing, it indicates that the market’s capacity to absorb trillion-dollar landmark IPOs is nearly saturated. This will directly affect the difficulty of securing anchor investors and the pricing ceiling for OpenAI’s roadshow in September.