Inside Stanford’s AI Gold Rush: 100 + Student-Led Start-ups Signaling the Next Big Wave

1、Executive Summary

Over the past 30 days Stanford’s campus once again morphed into a micro-cosm of the global hard-tech AI boom. More than 100 venture projects were pitched across internal demo days and local accelerators, spanning ten high-momentum tracks from healthcare and robotics to climate tech and consumer AI. Fund-raising data confirm that capital is rotating back to “AI + deep-tech” themes: global digital-health investment hit $6.3 billion in Q1 2025, 60 % of which targeted AI solutions , while Robotics-as-a-Service (RaaS) is forecast to expand 25 % CAGR to $125 billion by 2034 (marketresearchfuture.com).

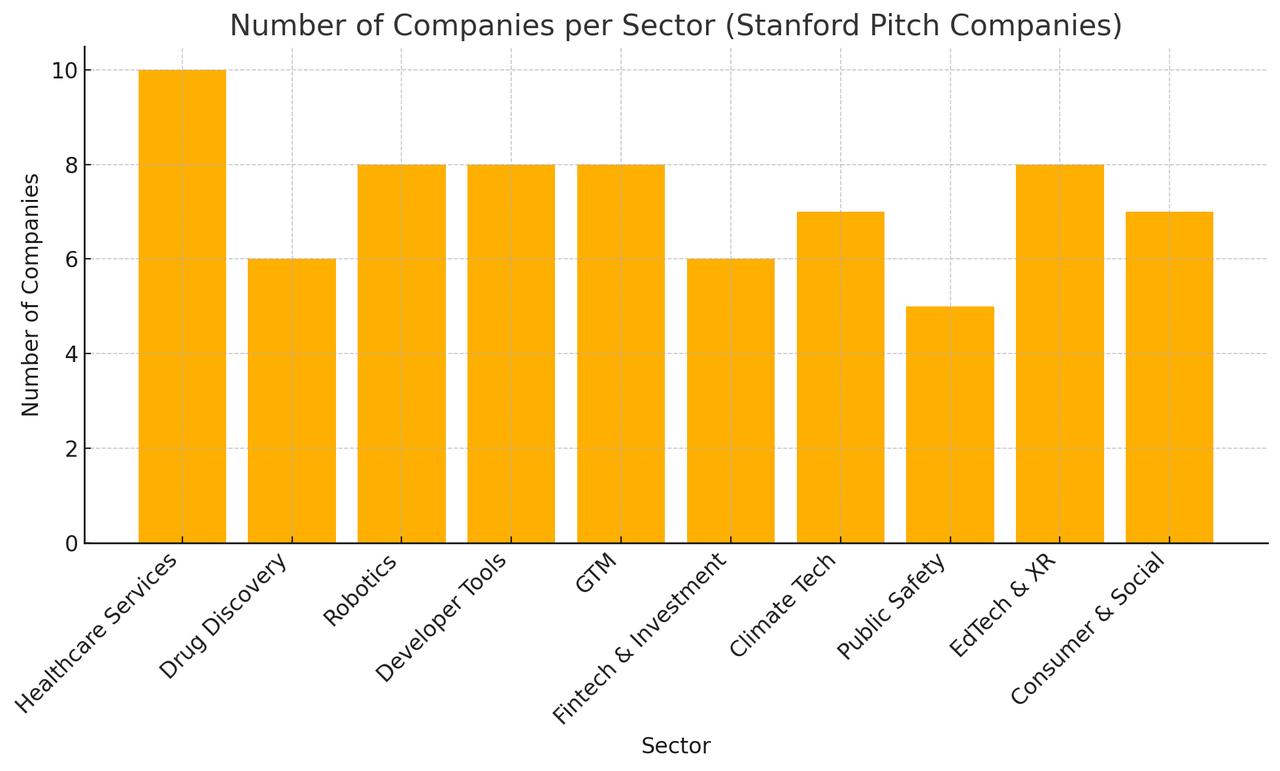

SVTR analysts mapped each Stanford pitch to one of ten sectors, counted the companies, and visualised the result. “Healthcare Services”, “Developer Tools”, “GTM/Customer Ops” and “EdTech & XR” jointly account for one-third of the cohort, signalling that applied AI still captures the imagination of technical founders even as infrastructure and hardware regain investor appetite.

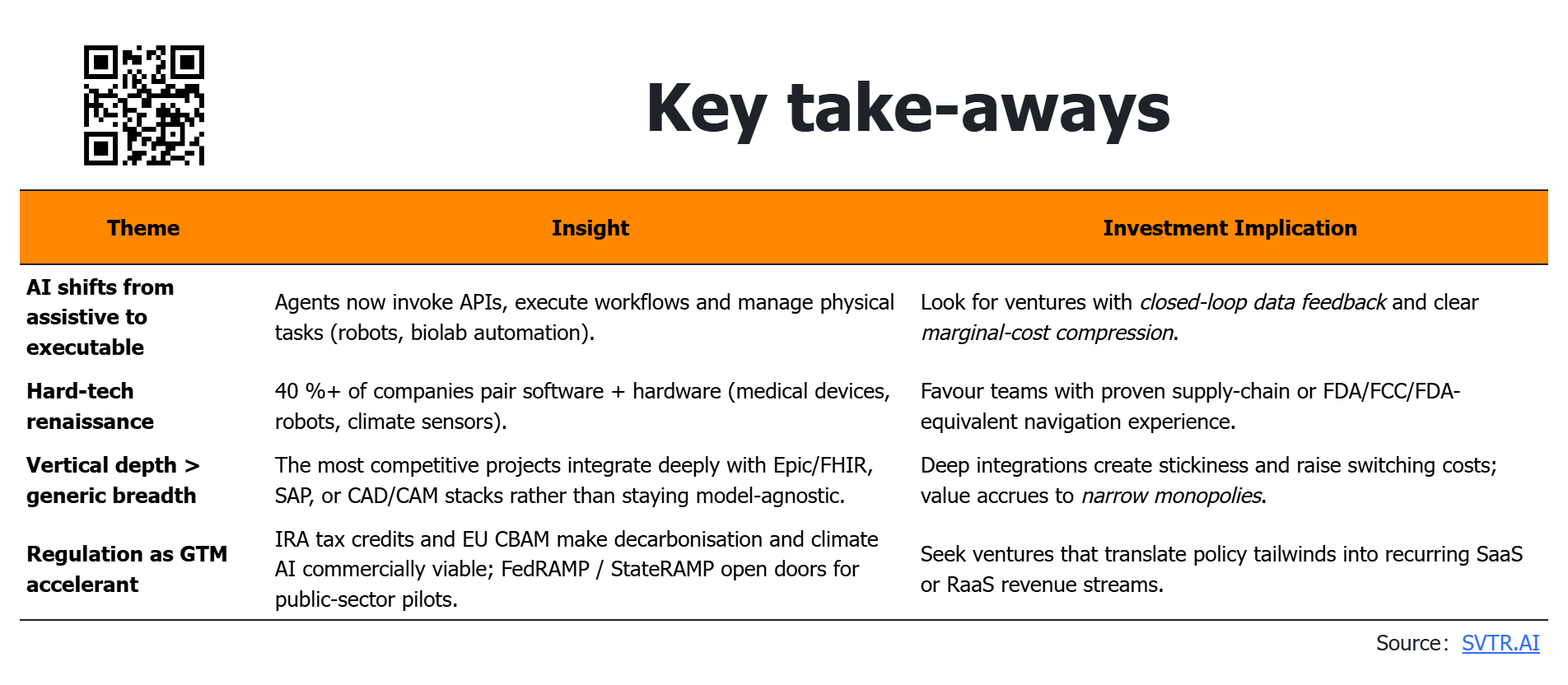

Key take-aways:

2、Methodology

Primary source: the master list of 100 + Stanford pitch companies shared during May–June demo events.

Secondary data: SVTR.AI venture database, Galen Growth digital-health tracker, Market Research Future (RaaS), Preqin 2025 VC outlook and public policy documents (IRA, CBAM) (galengrowth.com, marketresearchfuture.com, preqin.com, taxation-customs.ec.europa.eu).

Classification: ten tracks were defined to align with SVTR’s broader AI taxonomy. Counts were verified manually (see bar chart).

3、Sector Deep-Dives

Each subsection summarises market context, notable Stanford projects, illustrative deal highlights and SVTR commentary.

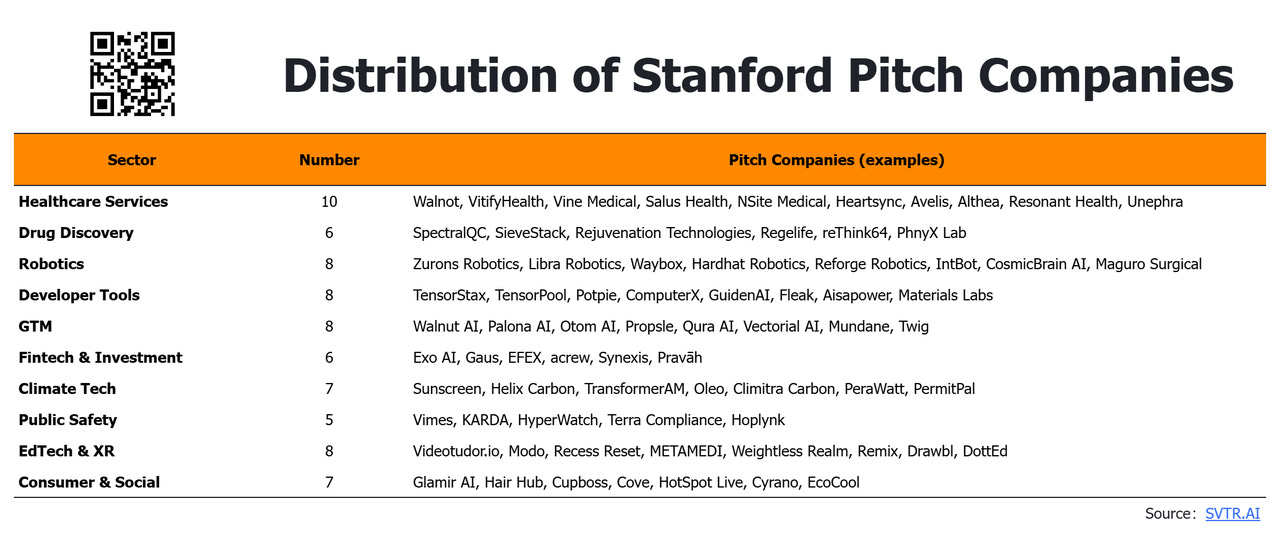

3.1 Healthcare Services (10 projects)

Market pulse

Global digital-health funding rebounded to $6.3 bn in Q1 2025; AI-enabled care delivery and clinical documentation captured 60 % of dollars, up 19 ppts YoY. Epic-integrated ambient scribe platforms dominate mega-deals (galengrowth.com). CMS has extended RPM reimbursement codes into 2025, lowering pay-lag risk.

Representative Stanford teams

Walnot – wireless fNIRS headband for in-home neuro monitoring.

VitifyHealth – NLP-driven patient-trial matcher; 40 % reduction in recruitment cycle.

Vine Medical – robotic intubation device with potential FDA “breakthrough” pathway.

SVTR outlook

Early-stage winners will (i) secure payer pilots or large IDN sandboxes, and (ii) offer fully managed FHIR/Epic adapters. EU MDR alignment is needed for trans-Atlantic scale.

3.2 Drug Discovery (6 projects)

Market pulse

AI-native small-molecule pipelines rank top-three in digital-health subsectors by capital raised. R&D cycles—historically 10 years / $2 bn—are shrinking through target-to-IND automation.

Representative Stanford teams

SpectralQC – combines quantum computing with generative chemistry to unlock “undruggable” pockets.

reThink64 – thermostable mRNA delivery platform mitigating cold-chain cost.

SVTR outlook

Regulatory risk is paramount; favour ventures partnered with CROs or pharma co-dev deals providing wet-lab validation and data exclusivity. Hybrid compute + lab automation skill sets will outperform pure-play model shops.

3.3 Robotics (8 projects)

Market pulse

Global RaaS is projected to reach $125 bn by 2034, 25 % CAGR (marketresearchfuture.com). Hardware margins must outrun depreciation. Subscription models (opex vs capex) ease buyer adoption.

Representative Stanford teams

Zurons Robotics – autonomously patrols apartment complexes; pilot in Oakland.

Libra Robotics – PV-panel installation bot vs >15 % EPC labour share.

Hardhat Robotics – “robotic apprentice” trains via imitation + reinforcement; rental + SaaS maintenance revenue.

SVTR outlook

Series A investors look for >35 % unit gross margin and evidence that post-sale service can be delivered remotely. Integration with OSHA / CE certifications accelerates enterprise uptake.

3.4 Developer Tools (8 projects)

Market pulse

GPU spot-rates for Nvidia H100 dropped below $2/hr; platforms such as TensorPool advertise 50 % lower opex than Hyperscale IaaS. AI assistants are shifting from code-completion to auto-commit agents.

Representative Stanford teams

TensorStax – deterministic agent that heals failed Airflow/DBT DAGs.

Potpie & ComputerX – desktop workflow agents for semi-technical founders.

SVTR outlook

Multi-cloud GPU schedulers plus open-weight model hubs will stratify winners. EU AI Act transparency rules heighten the value of provenance tooling and dataset audit features.

3.5 GTM / Customer-Ops (8 projects)

Market pulse

Sales / support remains the fastest path to positive ROI for GenAI: cost-to-serve drops 60 – 80 %, CSAT rises double-digits in early deployments. Voice + multimodal agents unlock SMS, telephony and email in one stack.

Representative Stanford teams

Palona AI – $10 m seed; high-EQ multimodal agent across voice/SMS/email.

Walnut AI – grafts AI co-pilot onto professional network graph.

Vectorial AI, Otom AI – embed LLM insights into Jira & CRM.

SVTR outlook

Procurement hinges on privacy posture (Bring-Your-Own-CRM) and explainability. Vendors that tie agent output directly to revenue or ticket-deflection metrics can command usage-plus-outcome pricing.

3.6 Fintech & Investment (6 projects)

Market pulse

Preqin expects a deal rebound in 2025 as rate cuts unlock liquidity, and LPs increasingly back “efficiency tools” in investment workflows (preqin.com). AI augments, not replaces, human analysts—time-to-model compresses from hours to minutes.

Representative Stanford teams

Synexis – real-time AI analyst scrapes private-company data, matches term-sheets.

Exo AI – autonomous agent for granular risk pricing.

SVTR outlook

Competitive moat = proprietary financial/talent graph + interpretability dashboards for compliance. Sandboxed deployments (on-prem VPC) are table stakes for regulated asset managers.

3.7 Climate Tech (7 projects)

Market pulse

IRA tax credits and EU CBAM have created explicit revenue accelerants for decarbonisation projects (pv-magazine-usa.com, taxation-customs.ec.europa.eu). Over 62 % of disclosed climate funding YTD 2025 targeted mitigation & efficiency.

Representative Stanford teams

Sunscreen – micro-fog cooling to cut crop water use 25 %.

Helix Carbon – in-situ CCU module for steel mills; converts CO₂ to syngas.

TransformerAM – additive-manufactured transformer cores boosting grid efficiency.

SVTR outlook

Hardware CAPEX is heavy—government grants, strategic CVC or project-finance vehicles often complement VC. Teams that pair policy fluency with tech depth out-execute.

3.8 Public Safety (5 projects)

Market pulse

National security start-ups shorten deployment cycles from decades to months; FedRAMP and StateRAMP define software compliance gates. Procurement still runs 9-18 months.

Representative Stanford teams

Vimes – cross-agency crisis-intervention platform; cuts response delay from 40 days to 12 h.

KARDA – auto-generates body-cam incident reports.

SVTR outlook

SaaS + integration fees is winning model. Early alignment with CJIS, ITAR and ethical AI audit frameworks de-risks later stage bids.

3.9 EdTech & XR (8 projects)

Market pulse

With GPT-4o and Apple Vision Pro releases, “immersive + personalised” learning overtakes MOOC 1.0 content. Investors value DAU retention over total enrolled headcount.

Representative Stanford teams

Weightless Realm – glasses-free 3-D hardware for surgical simulation.

Remix – 2-D to 3-D live stream engine.

Videotudor.io, Modo – AI tutor chatbots reducing non-tech founder learning curve.

SVTR outlook

Hardware plays must validate latency and comfort metrics; software platforms need path to district-level budgets (K-12) or employer-sponsored upskilling spend.

3.10 Consumer & Social (7 projects)

Market pulse

GenAI is reshaping user-generated content, NPCs and social graphs. Monetisation leans on in-app purchases or revenue share with creators.

Representative Stanford teams

Glamir AI – real-time AR make-up recommender.

Cove, HotSpot Live – AI-curated local events and hobby tribes.

SVTR outlook

Unit economics hinge on CAC vs repeat spend; international DTC expansion (Asia-Pac, LatAm) tests retention of culture-specific AI assistants.

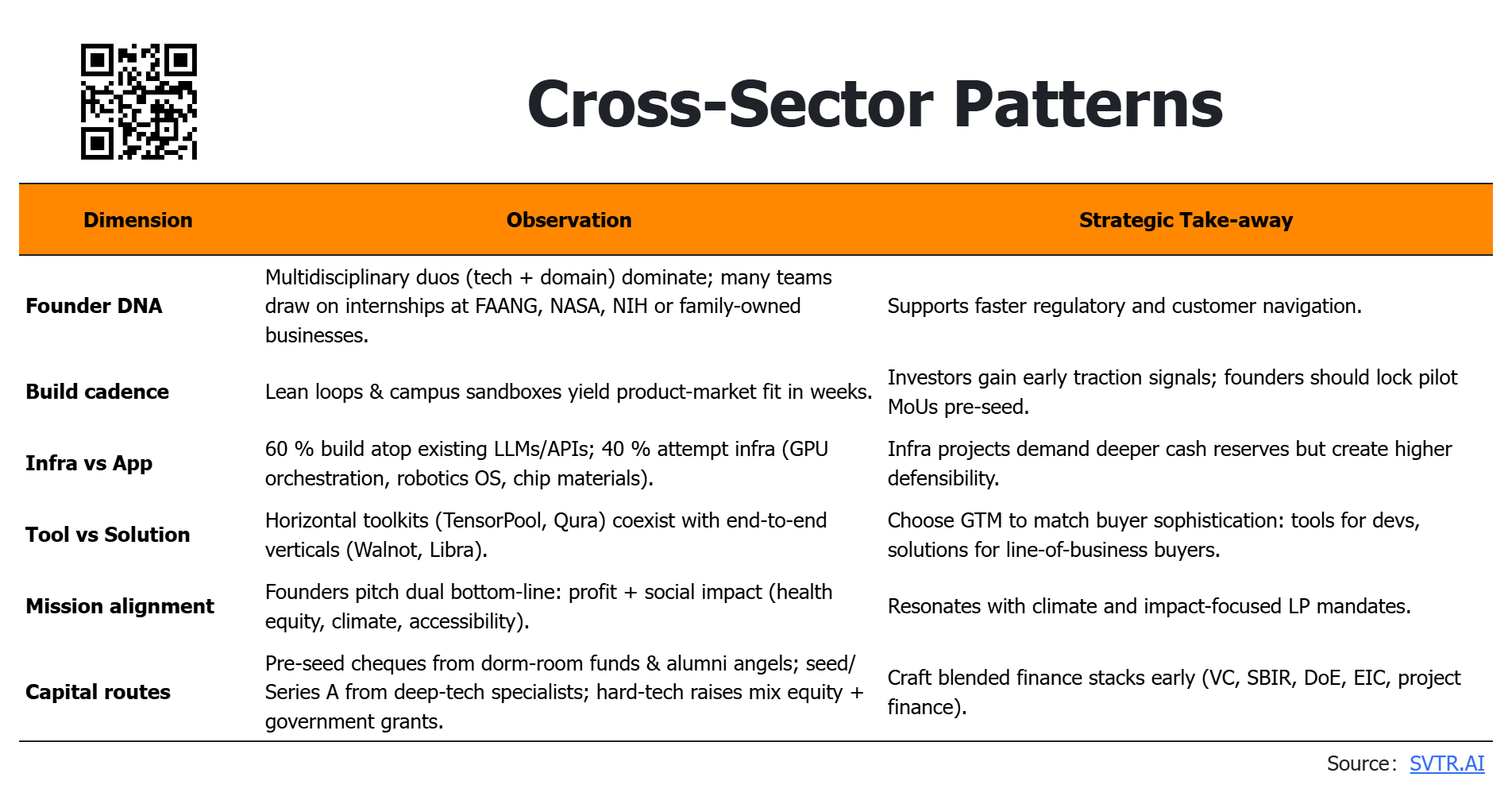

4、Cross-Sector Patterns

5、Outlook & Recommendations

For Founders

Prioritise regulatory-ready architecture—FHIR, FedRAMP, CBAM or EU AI Act alignment shortens enterprise sales by quarters.

Embed closed-loop data capture; models without proprietary feedback risk commoditisation.

Design capex-lite pilots—RaaS or usage-based GPU credits lower customer friction.

For Investors

Hard-tech valuations now account for IRA/CBAM subsidies—model blended IRRs including tax credits.

Underwrite GPU cost sensitivity and multi-cloud arbitrage when diligencing dev-tool plays.

Assess explainability layer in financial & safety-critical AI—expected to become mandatory.

For Corporate Partners

Leverage Stanford pipeline for innovation sprints; many teams seek design-partners rather than pure capital.

Offer data partnerships—early access to domain-rich datasets is decisive in model fine-tuning.

6、Appendix

Acknowledgements

SVTR.AI thanks Stanford Founders, Breakthrough and Llama Lounge for access to on-campus pitch sessions, and the 100 + founders who shared data and demos.

Prepared by the SVTR.AI Research Team | Published 4 June 2025