Goodwater and the application-layer bet

Everyone is pricing the AI model layer. Goodwater spent a decade pricing the opposite bet.

Goodwater Capital calls itself the world's largest pure consumer-tech VC — ~$3.3B AUM, 79 companies across 19 countries, ~60% in seed and early stage. Its thesis, in co-founder Chi-Hua Chien's words: the biggest winners of the AI era won't sell AI. So it deliberately skips models and compute, and backs consumer applications only.

The historical logic. Chien repeats one rule to LPs: value accrues to the application layer, not infrastructure. Internet era — infrastructure created ~$400B in market cap, applications ~$3.1T. Mobile — infrastructure ~$700B, applications ~$3.7T. Netflix, Meta and Uber all grew on pipes someone else laid.

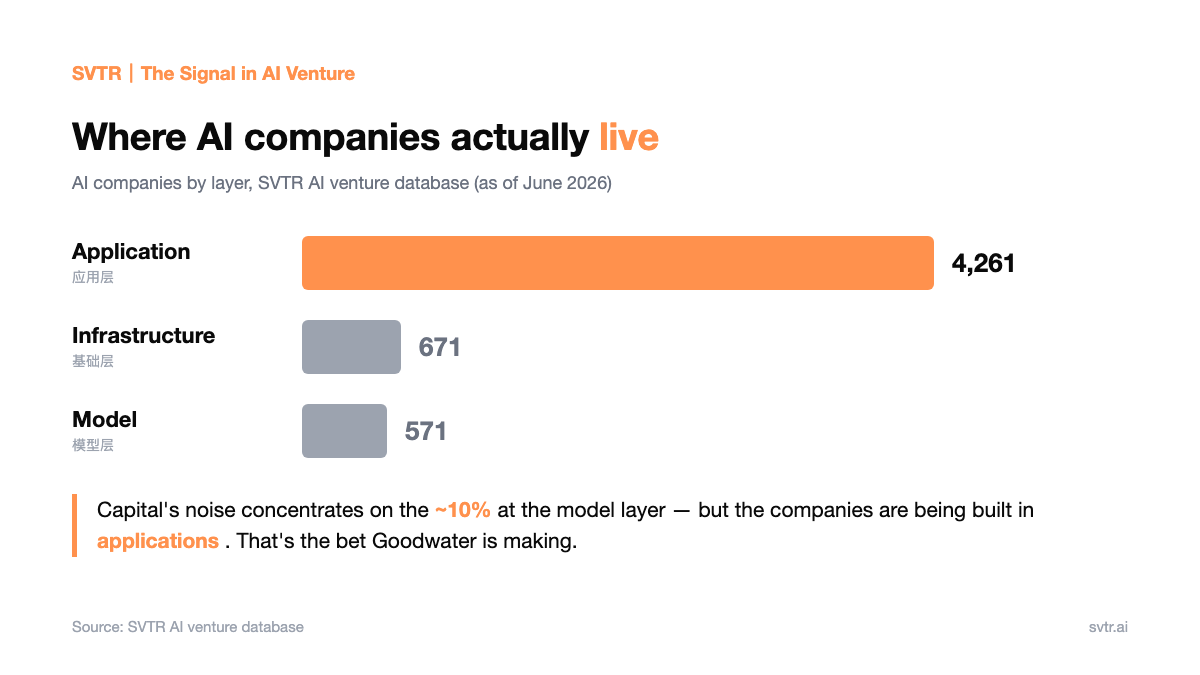

That distribution is showing up in our own data. Per SVTR's AI venture database, among the AI companies we've tiered, the application layer holds 4,261 companies vs. 571 at the model layer and 671 at infrastructure (as of June 2026). Capital's volume concentrates on that ~10% of model companies; the density of companies actually being built sits in applications. Goodwater is betting that AI won't flip this.

The AI twist: capital efficiency. In 2023 Goodwater raised over $1B in one shot, ~60% for seed and early. The assumption: AI lets application companies hit revenue and margins with tiny teams, so the unit economics of an early check are better than in the last consumer cycle. Chien also leaves infrastructure investors a sharper warning — the capability gap between on-device AI and cloud frontier models was 18–24 months two years ago, is ~6 months now, and he expects it to compress to 3 within a year. Once it closes, the model layer's differentiation commoditizes faster than most expect.

The portfolio: from giant exits to a "personalization" bet. Goodwater's past exits were mostly absorbed by incumbents: Musical.ly (acquired by ByteDance for >$1B in 2017, folded into TikTok), Photomath (Google), Dosh (Cardlytics), Care/of (Bayer). Still-held names span the globe — Monzo in the UK, Toss Bank in Korea. This cycle's AI bets are the part to watch: 22 deals since 2023, almost all seed and early, across entertainment, office, tax, healthcare and finance. Read AI raised twice in 2024 ($21M A, then $50M B six months later); the largest is Stash ($146M H round, 2025). Chien calls the theme "personalization" — entertainment apps doing $100M–$600M ARR at high margins where users don't feel they're using AI; MIDI Health using AI to widen the supply of doctors for perimenopausal hormone therapy. His most contrarian line is "offline reconnection": he backed Fever (a "European Live Nation"), betting that the more infinite digital content becomes, the scarcer and more valuable real-world gatherings get.

The quiet tell. 8 of those 22 deals were co-invested alongside Y Combinator in the same round; Lightspeed and Madrona twice each. So nearly a third of its early bets sit downstream of YC's already-filtered consumer funnel — its real edge is likely less "unique discovery" than judging which app's user retention can survive the giants, and daring to bet early in emerging markets.

The risks — all on one assumption. Consumer-AI moats are thin and get thinner as model capability spills over; differentiation falls back on distribution and brand, the incumbents' home turf. Exits depend on overseas M&A and IPO windows (Getir kept losing money; Monzo had turbulent years), and emerging-market liquidity is more cycle-dependent. And the women's-health / voice / offline-reconnection directions are early signals, not yet proven markets big enough to return a large fund.

Why it matters for cross-border investors. Betting on the application layer is nearly consensus. The hard part is whether the winners are startups at all. When capability is everyone's, the game returns to distribution and user relationships, where Meta and Google already sit. The next 18 months are the test: watch which of Goodwater's bets the giants absorb, and you'll know how deep its moat really is. In China the question barely breathes. Consumer innovation is internalized by ByteDance, Tencent and Alibaba, yet Goodwater is already entangled with Chinese capital (Musical.ly went to ByteDance; portfolio name Weee! serves North American Chinese). Read it as an observation post: watch which country its next seed check lands in.

Sources: SVTR AI venture database (Goodwater record, 22 AI deals, AI company tiering) · Goodwater 2023 fundraise & site · StrictlyVC / TechCrunch interviews with Chi-Hua Chien (June 2026).